See also

24.03.2025 10:23 AM

24.03.2025 10:23 AMGlobal financial markets continue to swing back and forth amid uncertainty over the actual impact on the economies of various countries targeted by Donald Trump's tariff hikes, which have prompted retaliatory measures in return.

The spring corporate earnings season in the U.S. is going relatively well. Overall, companies are reporting positively, which should instill optimism among investors. However, this has not translated into a consistent upward movement in the indices. The persistent focus on tariffs pushed by the U.S. president remains the main reason, as Trump continues using aggressive geopolitical tactics to force his key trading partners to foot the bill for America's economic recovery. Despite this, the stock market has managed to stay afloat, as corporate earnings show, but recent economic activity data—particularly in manufacturing—have done little to inspire further optimism.

Today's release of PMI data for the manufacturing and services sectors is particularly noteworthy. According to consensus forecasts, the U.S. Manufacturing PMI is expected to slow from 52.7 to 51.9 in March. However, it is still projected to remain above the 50-point threshold, signaling continued expansion in the U.S. real economy. Meanwhile, the Services PMI is expected to rise from a preliminary 51.0 to 51.2, which would also be a positive sign—assuming the figures meet or exceed expectations.

The tariff issue appears to be nearing its peak, with April 2 marking the deadline for Trump to implement his promised sweeping import duties. Interestingly, futures on the three main U.S. stock indices opened with an upward gap today, indicating that markets have already priced in the tariff topic. At the same time, investors believe that Trump may not follow through with the tariffs. As mentioned earlier, his goal is to pressure trade partners into paying more than the U.S. does, thereby reducing the trade deficit and easing the fiscal burden—steps that would undoubtedly support domestic economic growth.

If today's PMI reports meet or exceed expectations, they could provide local support for the U.S. stock market, which may also benefit global equity indices. And if the April 2 tariffs are delayed or softened, a rebound in the U.S. stock market this week could turn into a more significant rally, accompanied by a strong upside in major stock indices.

This scenario seems realistic, provided the PMI data show positive momentum. That would help calm investors' fears of an imminent recession in the U.S. economy.

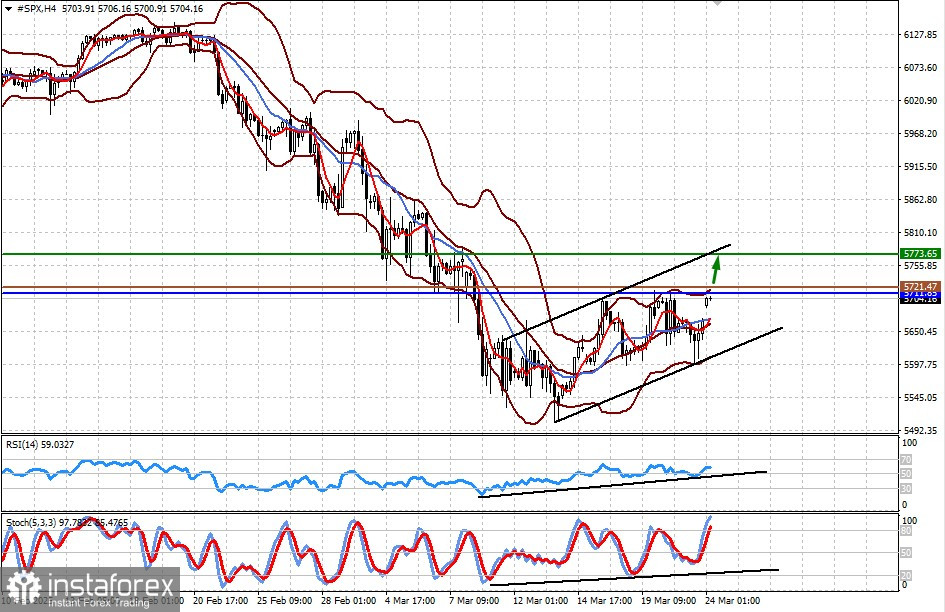

The CFD contract for S&P 500 futures opened with a gap up today, signaling a positive market outlook ahead of key PMI reports. If the data meets expectations or shows further growth, the contract may rise. A breakout above the resistance level at 5711.85 could lead to an increase towards 5773.65, with an entry point suggested at 5721.47.

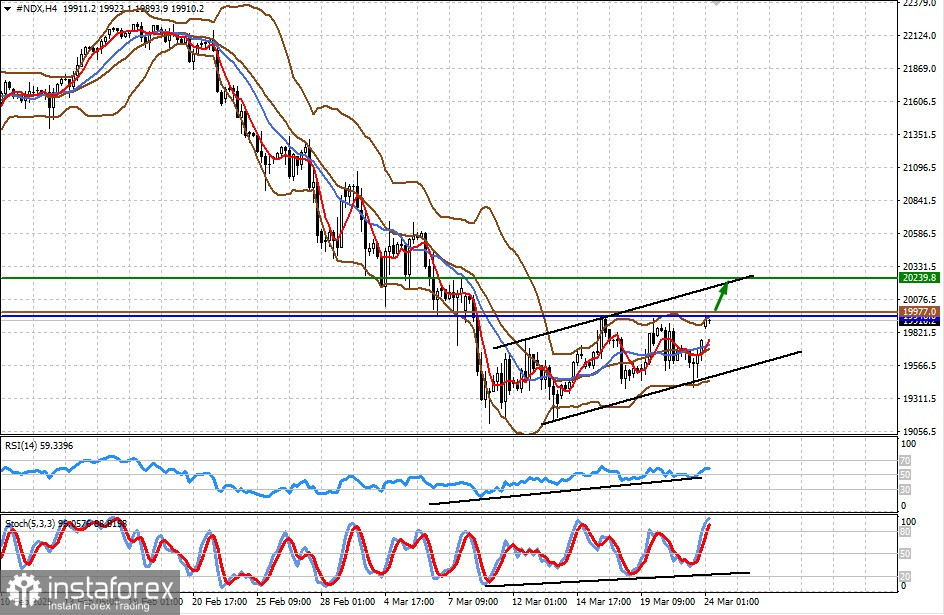

#NDX

For the NASDAQ 100 futures, the CFD contract also opened with a gap up, reflecting optimistic expectations surrounding today's key PMI data. If the figures meet or exceed forecasts and show upward momentum, this could boost demand for the contract. A potential target could be set at 20239.80 upon breaking through the resistance at 19946.00, with an entry point suggested at 19977.00.